What Is Credit Card?

Credit card is a small plastic or metal card that lets you borrow money from a bank to buy things. You can use it to pay for shopping, food, travel or other services. The money you spend is not taken from your bank right away. Instead, you borrow it from the card company and pay it back later.

If you pay after the due date, you may have to pay extra money called interest. Some cards also have a yearly fee. Popular credit card companies are Visa, Mastercard, American Express and Discover. Many banks and credit unions also give their own credit cards.

Credit card can be helpful when your bank account has less money or when you want to buy something expensive and pay for it slowly.

Types of Cards

There are different kinds of cards that people use to buy things – credit cards, debit cards and prepaid cards.

All of them look almost the same but they work in different ways.

1. Credit Cards

When you use Credit card, you are borrowing money from the bank. You must pay it back later. If you don’t pay the full amount on time, the bank will add interest and extra charges.

Credit cards can help you build a good credit history if you use them carefully. They also give you extra protection if something goes wrong with a purchase.

Your credit score decides what kind of credit card you can get and what interest rate you will pay.

2. Debit Cards

A debit card is directly linked to your bank account. When you buy something with it, money is taken out of your account right away.

Debit cards are good for daily use but do not give the same protection as credit cards if someone steals your card or if there is a problem with a purchase. That is why people often use credit cards for big or online shopping.

3. Prepaid Cards

A prepaid card is not connected to any bank account. You first add money to the card and then you can spend only that much.

You cannot spend more than the money you have loaded. Some prepaid cards work everywhere like Visa or Mastercard.

Others, like store gift cards or salary cards, work only at certain places.

4. Rewards Credit Cards

Some credit cards give you rewards every time you buy something.

You can get cashback, travel points or shopping offers.

These cards are good for people who pay their bills fully every month.

If you don’t pay on time, the interest will be more than the rewards you earn.

How Do Credit Cards Work?

Credit card lets you buy now and pay later.

Every card has Credit limit, which is the maximum amount you can borrow.

When you buy something, that amount is added to your balance and your available credit becomes less. When you make a payment, your available credit goes up again.

You can keep using your card as long as you stay within your credit limit.

But if you do not pay your full balance every month, you will have to pay interest on the remaining amount.

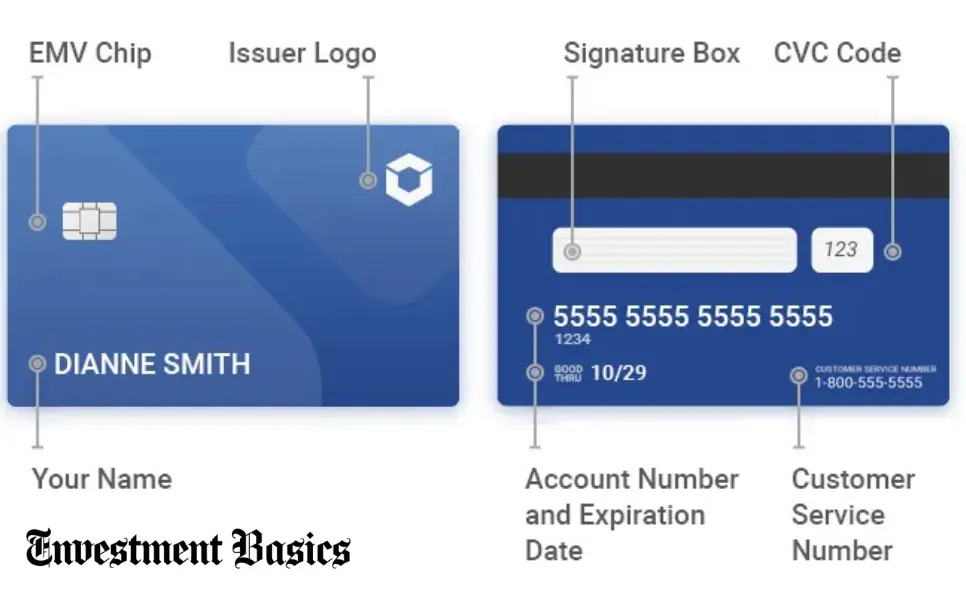

What’s on Credit Card?

Credit card has several small details printed or written on it.

Each part has a special use.

- Issuer Logo: The name of the bank or company that gave you the card (like Chase or Capital One).

- Payment Network Logo: The symbol of the payment network, such as Visa, Mastercard, Discover or American Express.

- EMV Chip: A small metal chip on the card that helps you pay safely in stores.

- Contactless Symbol: Some cards let you tap instead of swiping. The symbol looks like a Wi-Fi signal.

- Magnetic Stripe: The black strip on the back that holds your card information.

- Your Name and Card Number: Your name and a unique number printed on the card.

- If the number starts with 3, its American Express.

- If it starts with 4, its Visa.

- If it starts with 5, its Mastercard.

- If it starts with 6, its Discover.

- Expiry Date: Shows the month and year when your card will stop working.

Before that, your bank will send you a new one. - CVV Code: A 3-digit (or 4-digit for Amex) security number used for online payments.

- Customer Service Number: A phone number on the back to call if you have a problem or question.

- Signature Box: A small area where you sign your name.

Pros and Cons of Credit Cards

Every good thing has two sides – good and bad. Credit cards also have many benefits but also some risks if not used carefully.

Let’s look at both.

| Pros (Good Things) | Cons (Bad Things) |

|---|---|

| Helps you keep track of where your money goes | Some cards have extra fees that can add up |

| Gives you rewards like cashback or points | If you don’t pay the full amount, interest can be very high |

| Easier and safer to carry than cash | Sometimes, its not clear how to get approved |

| Can help you build a good credit score | Can hurt your credit score if you spend carelessly |

| You can avoid paying interest if you pay the full bill on time | Interest rates can change any time |

| Many cards give extra benefits and discounts | Paying only the minimum amount each month can lead to big debt |

Should You Get Credit Card?

Getting Credit card is a personal choice. It depends on your money habits and goals. Here are some times when getting Credit card can be a good idea:

- You want to build a good credit score.

- You can pay your bill in full every month.

- You want to earn cashback, points or travel rewards.

- You want extra safety when shopping, especially online.

But it may not be a good idea to get Credit card if:

- You often spend more than you should.

- You are worried that you might get into debt.

Remember, Credit card can be your friend or your problem – it depends on how wisely you use it.

Wanna Know What Does Finance Mean?

How to Choose the Right Credit Card

Choosing the best credit card is not about picking the first one you see.

You should take some time to find the card that matches your needs.

Here are some easy steps to follow:

1. Check Your Credit Score

Your credit score shows how well you manage your money.

If your score is high, you can get better cards with more benefits.

If your score is low, you may have fewer options.

2. Look at Your Spending Habits

Think about where you spend most of your money.

If you spend more on food, travel or fuel, choose card that gives rewards in those areas.

Some cards give extra cashback or points for certain purchases.

3. Know What You Want in card

Decide what is most important to you:

- Do you want cashback or travel points?

- Do you want card with 0% interest for a few months?

- Do you travel often and need airline or hotel perks?

- This helps you find card that fits your lifestyle.

4. Compare Different Cards

After knowing what you want, compare many cards before choosing one.

Check their fees, interest rates and rewards.

- If your credit score is high (usually 670 or above), you will find more options.

- If your score is lower, don’t worry – start small and build it up.

5. Apply for the Card

Once you choose the best one, you can apply:

- On the bank’s website,

- By phone, or

- At a local bank or credit union in person.

Learn About Banking

How to Get Credit Card for the First Time

If this is your first credit card, you might not get many choices at first.

But don’t worry – there are still good options for beginners. Here’s what to do:

1. Pick the Right Type of Card

If you are a college student, go for a student credit card. It usually has simple rules and no deposit. If you are not a student, you can try a secured credit card. For this, you pay a small security deposit that acts as your credit limit.

Some banks also offer debit-credit mix cards that are easy to manage.

2. Compare the Card Features

Beginner cards may not give big rewards but still check:

- Interest rate (APR)

- Annual or monthly fees

- Any small cashback or benefit

Choose card that helps you learn and manage money easily.

3. Avoid High Fees

Some cards for beginners have very high fees.

Try to avoid cards that charge:

- Monthly fees

- Setup or processing fees

- High annual charges

Many banks have free cards with better terms. Pick those.

4. Build Good Credit Habits

When you get your first card:

- Use it for small purchases only.

- Pay the full amount on time.

- Keep your credit use low (don’t spend all your limit).

Doing this will help you build a strong credit score and soon you can qualify for better cards.

Also Checkout What will You do to Maximize on Your Postsecondary Education Investment?

Conclusion

Credit card can be a very helpful tool when you use it with care. It gives you comfort, safety and many rewards but it also needs responsibility. Always remember that the money you spend on Credit card is borrowed money that you must pay back on time. If you pay your bills fully each month, you can enjoy all the good parts without falling into debt. But if you spend carelessly, it can cause stress and extra charges.

So, use your credit card wisely, keep track of your spending and make your payments on time. When used the right way, Credit card can make your financial life easier and help you build a strong credit future.

Ethan Caldwell is a seasoned financial analyst and journalist with over a decade of experience covering global markets, investment trends and personal finance strategies. As contributor to leading financial media platforms, Ethan simplifies complex economic insights into practical advice for everyday investors. His expertise spans stock market analysis, fintech innovation and wealth management. When he’s not decoding Wall Street trends, Ethan enjoys mentoring young entrepreneurs and exploring data driven approaches to sustainable investing.